Is Your Accounts Receivable Normal? Here's How to Actually Know

- Maleeka Catlin

- 11 hours ago

- 4 min read

Ask a business owner how their sales are doing, and they'll have an answer in seconds. Ask them how their receivables compare to other companies in their industry, and most will just shrug. It's not that they don't care — it's that almost nobody benchmarks it. There's no dashboard alert for "your unpaid invoices are aging worse than your competitors'." There's just a slow, quiet drift that feels normal because nobody ever showed you what normal actually looks like.

That's the problem with this particular blind spot: it doesn't announce itself. Revenue looks fine. The business looks healthy. And underneath, a growing share of that revenue is sitting in accounts that may never convert to cash.

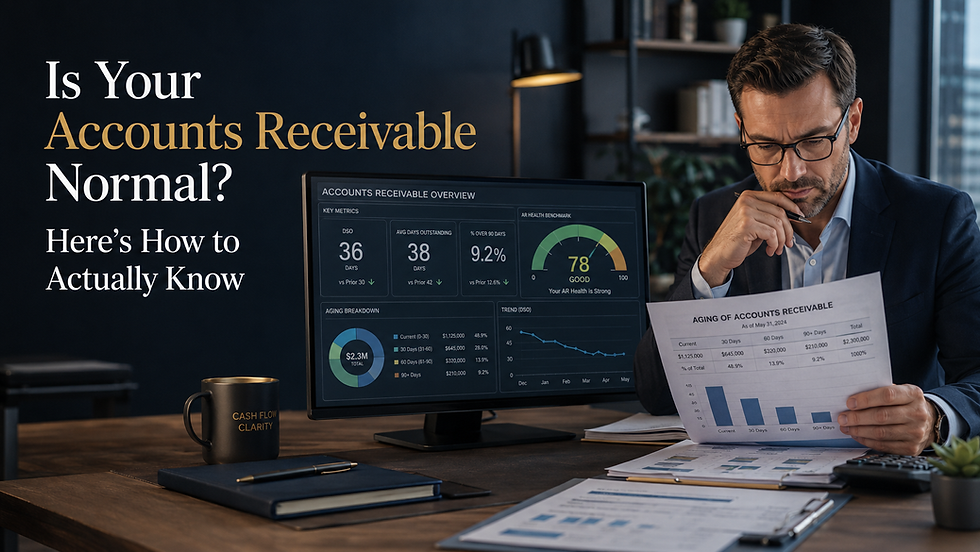

The metric that actually matters: DSO

Accountants call it Days Sales Outstanding, or DSO — the average number of days it takes your business to collect payment after a sale. The formula is simple: divide your accounts receivable by your total credit sales, then multiply by the number of days in the period you're measuring. What it tells you is not simple at all. A rising DSO means your customers are, on average, taking longer to pay — and every extra day represents cash that's owed to you but isn't available to run your business.

A related number worth knowing is Average Days Delinquent, or ADD — how many days past due your invoices are, on average, compared to your ideal collection speed. If your DSO is high but your ADD is low, your business simply operates on longer terms (not necessarily a problem). If your ADD is climbing, that's a more specific signal: your customers aren't just paying on your terms slowly, they're paying later than even your own terms allow.

Neither number means anything in isolation. The only way to know if yours is a problem is to compare it to your industry.

What "normal" actually looks like right now

This is where most business owners are working blind, and the real numbers are more sobering than most expect. Nationally, close to half of small businesses report having invoices more than 30 days past due, and a significant share — roughly two-thirds by some measures — have invoices sitting 90 days past due or longer. More than one in ten have invoices aged past 120 days, the point where recovery starts becoming a genuinely different conversation than it was 60 days earlier.

The picture also shifts sharply by industry. Office and facilities management companies report average payment waits north of 100 days. More than half of manufacturing suppliers report late payments averaging close to two months. Security and compliance-related services see a large share of their overdue invoices sitting past the 90-day mark. A company in one of these industries comparing itself to a flat, generic "30-day" assumption isn't just uninformed — it's measuring itself against the wrong yardstick entirely.

This is exactly why a flat "pay within 30 days" assumption is often the wrong yardstick. A construction supplier and a professional services firm do not have the same normal, and treating them as if they do leads business owners to either panic over receivables that are actually typical for their industry, or — more dangerously — dismiss receivables that are genuinely a warning sign because "everyone's a little behind."

Why this number predicts trouble before it's visible elsewhere

A rising DSO or ADD rarely shows up as an emergency. It shows up as a series of small, explainable decisions: paying a supplier a few days later than usual, holding off on a hire, using a credit line to smooth out a gap that used to smooth itself out. None of these individually looks like a crisis. Together, over a few quarters, they are the crisis — just one that arrived quietly enough that nobody flagged it in time.

This is consistent with what shows up across small businesses nationally: a large share say they've had to lean more on credit cards or lines of credit specifically because of late-paying customers, and a meaningful number have delayed paying themselves to keep the business solvent. None of it starts as a five-alarm event. It starts as a receivables number nobody was watching.

What to actually do with this number

Tracking DSO and ADD only matters if it changes a decision. Here's what a rising number should actually trigger:

Benchmark against your specific industry, not a generic 30-day assumption. Fair Capital's accounts receivable benchmarking data breaks down the percentage of accounts 30, 60, and 90+ days delinquent by industry, so you can see where your business actually stands rather than guessing.

Segment your aging report — the accounts sitting at 30 days need a different response than the ones sitting at 90. Waiting too long on the older bucket is usually where recoverable money quietly becomes unrecoverable. Our piece on the hidden cost of waiting to collect a B2B debt goes into why timing matters more than most businesses assume.

Set a real trigger point, not a vague one. If an account crosses 60 or 90 days with no payment plan in place, that should be a defined moment to escalate — not a judgment call made fresh every time. Our guide on when to send an account to collections lays out concrete signs worth watching for.

Review the trend, not just the snapshot. A DSO that's stable but high may just reflect your industry. A DSO that's climbing quarter over quarter, regardless of the starting point, is the more urgent signal.

The bottom line

Most businesses never check this number until it's already a problem serious enough to notice without checking. The ones that fare best treat it the way they'd treat any other vital sign — reviewed regularly, compared to a real benchmark, and acted on while there's still time to change the outcome.

If you want a clearer picture of where your business actually stands, Fair Capital's benchmarking data is a good place to start. And if that comparison turns up accounts that are already aging past the point of easy recovery, request a free quote and we'll help you determine the fastest realistic path to getting paid.

Comments